FX Daily Strategy: Europe, April 18th

Japanese CPI Continue to Moderate

Underlying weak JPY trend only likely to turn with lower US yields

GBP downside risks on retail sales

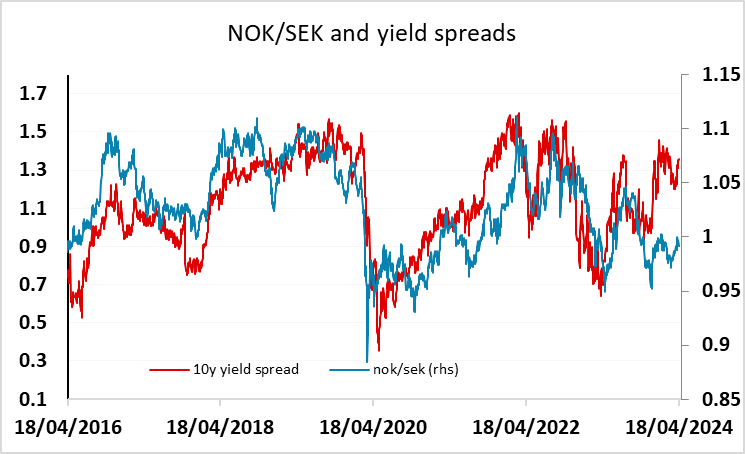

EUR/NOK due to turn lower

Japanese CPI Continue to Moderate

Underlying weak JPY trend only likely to turn with lower US yields

GBP downside risks on retail sales

EUR/NOK due to turn lower

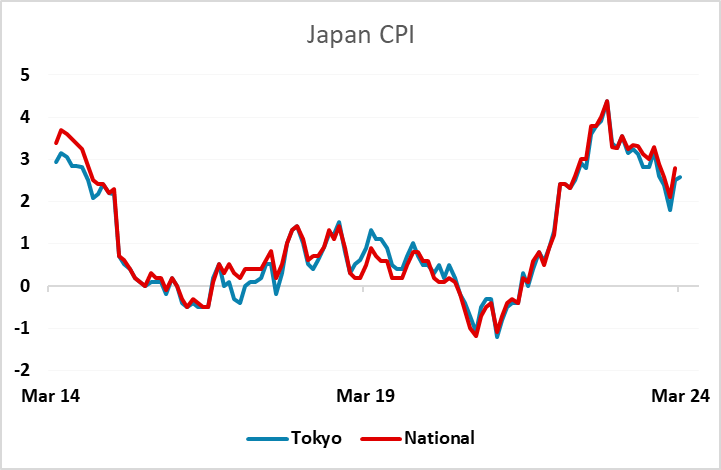

Japanese CPI and UK retail sales are the only data of significance on Friday. Usually, the national Japanese CPI data is well trailed by the Tokyo CPI data already released. But the Tokyo CPI numbers have been coming out a little below the national numbers of late, and there is some potential for this gap to be closed. So while Tokyo CPI inflation rose to 2.6% y/y in March from 2.5% y/y in February, the market consensus is for the national numbers to fall to 2.7% from 2.8%. This relates to base effects with a 0.4% rise in the national numbers last March against a 0.3% rise in the Tokyo index.

The Japan National y/y CPI coming in lower than estimate at 2.7%, ex fresh food 2.6%, ex fresh food and energy at 2.9%, all showing further moderation from February. We expect such moderation to continue throughout of the rest of 2024 with speed bumps in the coming month on wage spike. The BoJ's target of 2% has not been met and there is room for further policy changes in the coming months.

This could be significant for the JPY, which remained on the back foot through Thursday, with the market seeing the statement from the G7 and the tripartite statement from the US, Japan and South Korea on FX as underwhelming. While the statement didn’t rule out intervention, it suggested it would be reluctant, and participation from the US side remains unlikely. However, higher Japanese inflation would make resistance to further JPY weakness more likely. Even so, we continue to see JPY weakness as primarily a consequence of rising US yields and the implied decline in the equity risk premium. So although a stronger than expected Japanese CPI number could trigger some small JPY recovery, it will take a reversal of recent US yield rises to turn the weak JPY trend, both against the USD and the EUR.

UK retail sales have been choppy of late, but the underlying trend has been improving. Market consensus looks for another modest rise in March of 0.3%. However, this would cause a huge rise in the 3m annualised rate, due to the big December decline and subsequent January rise. This is of course possible, but the risks might be towards the downside. EUR/GBP has returned to the 0.8550-0.86 range after the more dovish comments from BoE governor Bailey on Wednesday, and may have potential to push up towards 0.86 if the data is on the soft side. However, the risks are not clearly one way, with seasonal factors often creating big distortions, and we doubt there will be a big market reaction. The BoE’s Ramsden and Mann are scheduled to speak on Friday. Mann will undoubtedly be hawkish, but Ramsden will have more potential for market impact.

Thursday saw some initial strength in the SEK, which produced a retreat from a test of parity in NOK/SEK. We continue to favour the upside in this pair based on the history of the correlation with the yield spread, but the move is likely to need to come from EUR/NOK, with EUR/SEK also looking too high relative to historic correlations.